Alternatives and Beyond – Fireside chat with Gripinvest

published By Aakanksha Sharma , February 20, 2024

Fireside chat with Nikhil Aggarwal – Founder & CEO of Gripinvest. You can read more about their latest funding round here – ET, Financial Express, VC Circle.

.

Congratulations on your latest round of $10M. How are the spirits in the team & what are the top few milestones you are looking to achieve with this round?

Raising capital is always great motivation for the team as it provides external validation of the business model as well as visibility of resources and time to expand. It has been even more meaningful to be able to secure this capital in a weaker funding environment, with a healthy appreciation in valuation and participation of 6 venture capital firms.

We are incredibly excited about the exclusive suite of investment products we offer, especially with 100% of our products being SEBI-regulated. We are now focused on driving growth in investment volumes led by higher awareness and delivering consistently great user experience. In the next 24 months, we aim to increase new investments enabled to 1,000 Cr annually and deliver at least 2 quarters of profitable operations.

Let’s talk about the space itself a little more. Alternative investments are still relatively new in the Indian context. Grip is amongst the pioneers in the space. In your 3-year journey, how have you seen the ecosystem evolve across demand, supply, VCs & distribution partners?

On all accounts, we have seen massive growth in the sector. The fact that SEBI has created two new licenses (OBPP and MSM REIT) to bring such alternative investments under regulatory purview is a sign of both the large opportunity as well as the evolution of this industry. Speaking more specifically:

- Demand: We estimate that digital alternative investment platforms collectively enabled over a billion dollars in investment last year. Since the introduction of the OBPP license (Online Bond Platform Providers) in Nov’22, SEBI has reported a 2x growth in retail investors in bonds. Across alternative investment platforms, we are seeing exponential growth in investment volumes

- Supply: When we started our business, large companies would often refrain from using platforms like ours to raise capital as they feared adverse public perception. However, now we actively speak to CEOs and CFOs who want to leverage our platform to create public awareness for their companies and brands by offering investment opportunities. In the last 6 months, we have listed investment opportunities for

- India’s second largest cash management company – a publicly listed corporate

- leading NBFCs like Navi, Ugro, Incred, Vivriti

- India’s largest cab fleet with a global blue-chip shareholder

- late-stage start-ups including unicorns on their way to IPO

- Distribution partners: While smaller distribution partners have been aggressively distributing alternative investments, we have recently started seeing larger institutions open to partnership. This trend is being accelerated now on account of

- regulatory clarity on several business models

- rising demand for affluent customers of these platforms

- a general view that diversification from equities may be advisable

- likely peaking of the yield curve which makes fixed-income investing even more attractive

- Venture Capital: Since most alternative investments being offered are fixed-income in nature, venture capital in the sector has also come from funds that deeply understand that market. Three of our equity investors – Anicut Capital, Stride Ventures, and Lighthouse Canton Nueva manage some of the largest debt funds in the country. The same is true for several other lead investors in other platforms – Kotak/ Strata, Zerodha/ Wint, Eight Roads (previously Fidelity)/ Wint. Venture Highway is a rare early-stage VC fund to have understood the opportunity in this industry as well as appreciated the attractive potential for servicing a rapidly growing affluent population. With regulations now in place, we expect VC interest in this sector to become more broad-based. At the same time, unregulated business models are unlikely to attract further capital.

One of the biggest reservations in this space has been around TAM. To further elaborate, there is a section that doubts the potential of alternatives to ever become a mass product, and consequently a large VC outcome. Having interacted with the customers closely over the last 3 years, what’s your take on that? How do you see TAM for alternatives in India?

The word ‘Alternatives’ is unfortunately a catch-all for everything other than gold, fixed deposits, and public equity. Should an AAA-rated fixed-income instrument, listed on the stock exchange and offered at INR 10,000 really be considered an alternative? Those are some of the products Grip offers. It is ‘Alternative’ because before this year it had never been offered to retail investors, but it is hardly exotic or risky, which is the general perception of alternative investments.

In understanding TAM, it is important to first appreciate the value proposition of products Grip offers vs. the generally perceived proposition of alternative investments. Grip offers secured, investment-grade rated, fixed-income options offering 10-16% IRRs. Retail investors today are seeking investment options between two extremes – safe FDs at 6% or the potential of 16% but volatile returns from the stock market. Grip is solving this gap in investment portfolios through its investment options.

Secondly, TAM for investment products is inversely related to the minimum investment amount. The higher the required minimum investment, the smaller the TAM. SEBI has recognized the need for enabling retail participation in such regulated products and accordingly has reduced the minimum investment amount by 90% from INR 10 lakhs to INR 1 lakh. It has proposed a further 90% reduction to INR 10,000. Furthermore, products offered through a public process can be offered at even INR 1,000. This reduction in investment amount has dramatically increased TAM.

The third factor in appreciating the large TAM this industry has is the changing demographic profile, driven by strong consistent economic growth. Multiple recent industry reports have identified that the ‘Affluent’ segment is likely to be the faster-growing segment. This is the core target market for our offerings.

You started with lease financing, and since then, a suite of products has gone live on the platform. Tell us more about your product strategy – product mix over the next few years, ticket sizes, & the key customer segments you will look to cater to with these products

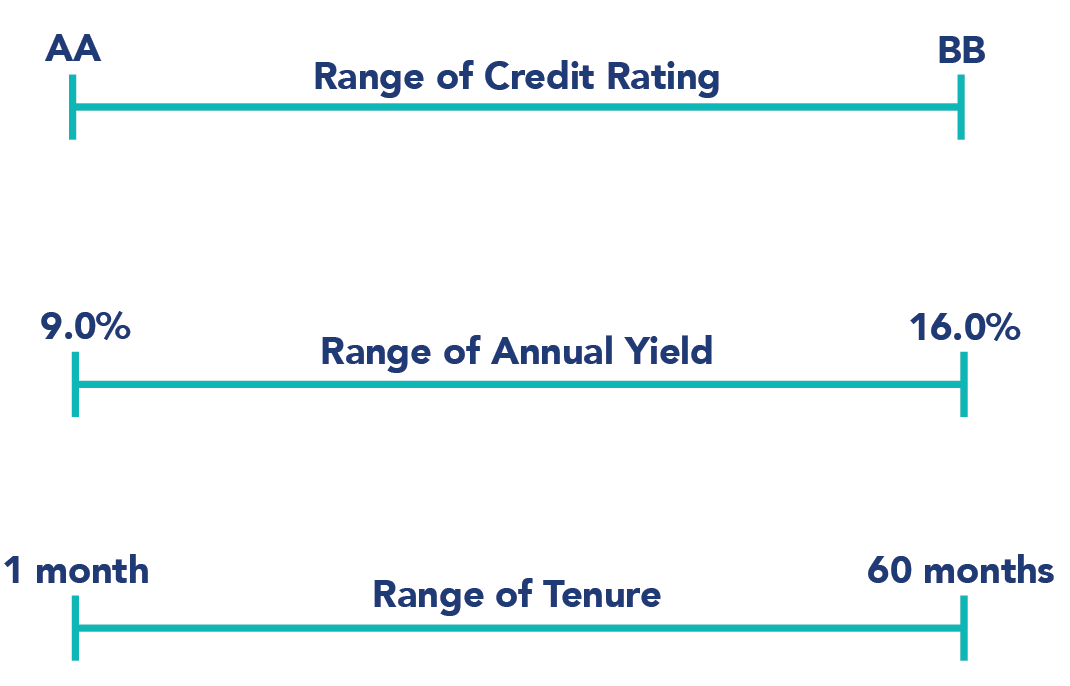

We realized very early that a single investment product is not what our customers want. Just as you don’t order the same cuisine on Swiggy or watch the same genre of content on Netflix, every investor is different and each investor wants to have the choice to build a diversified portfolio. This is also the first principle of investing and allows for healthier returns.

Our product strategy hence evolved around offering investment choices across risk, return, and tenure. The chart below represents the breadth of options a user has today on Grip.

Our addition of products over the last three years has been driven by our focus on completing this matrix of risk-return-tenure. The below table captures the products we offer and how they fit into the preferences of different investors

| Investment Product | Investor Objective |

| InvoiceX (Investing in a pool of invoices) | Short tenure < 12 months |

| LoanX (Investing in a pool of loans) | Medium tenure (12-18 months); High returns |

| LeaseX (Lease financing) | Long tenure (24-48 months); High returns |

| BondX (Investing in a pool of bonds) | Medium tenure (12-18 months); High credit rating |

| Corporate bonds | Medium tenure (12-18 months); High credit rating |

You have managed to consistently improve the take rates on the platform to a now-healthy number. Given the changes in the last year (structures included), are you confident to maintain/improve that? Do you think the margins will hold at scale and a large, profitable business can be built in this vertical?

Across products, whether soaps or investments, there are two types of business models in the world. Manufacturers and Distributors. Typically manufacturers have high margins because they build brand loyalty due to their differentiated products. With scale, these manufacturers are also able to reduce costs and have better supply chains. While distributors especially those who have limited product differentiation end up with tough competition and declining margins. Technology has made it possible for Manufacturers to also become Distributors and vice-versa, and those result in some of the strongest business models. Amazon-branded goods sold on Amazon are probably a great example and have the highest margin contribution.

We see Grip as a manufacturer of unique fixed-income products and also the primary distributor. With scale, we have seen the ability to reduce our cost of ‘manufacturing’ resulting in improving margins. I am excited about our ability to further improve margins led by establishing a strong brand and larger scale.

While alternatives may be fairly new, there are already a few scaled & upcoming wealth-tech platforms in India, both in B2B & B2B2C. And there are a couple in the alternatives space as well. How does Grip plan to stand out, capture mind/wallet share & build a brand? Do you plan to partner with some of these platforms?

We want to differentiate ourselves in terms of the investment options we offer and secondly in terms of the quality of user experience. On the former, we are clearly positioned as a high-yield platform offering 12-16% returns. At the same time, these returns are offered through products that have historically seen limited default rates and hence the risk-reward offered on Grip is unique. 80% of the investment options available on Grip are not available on any other platform.

On the latter, we believe that most Indian investors do not have access to high-quality wealth managers. They hence prefer to invest DIY and need to be provided an easy but powerful investment experience. Everything from discovery to payments to portfolio management must be intuitive, seamless, and secure. We have invested ahead of our peers in establishing a strong prod-tech team that has been first to market in launching features to achieve this. Among these features, I am most excited about launching the 1st SIP for fixed-income products in the country.

While 95% of investments on Grip today are facilitated on our platform, we do recognize the power of working with other scaled-up wealth-tech and wealth management companies offering more comprehensive portfolio management solutions. We are already integrated with several of them and in discussion with others. Carrying forward our tech-first approach, we have built a proprietary API stack that powers such integrations in a scalable manner.

Let’s also touch upon regulation, which has become the talk of the town in the fin-tech industry lately. We have seen the approach the regulators are taking – the most recent example being a sizeable investment platform that came into focus due to LLP structures. You have made regulatory compliance a top priority over the last 1.5 years – what led to that foresight & how do you plan to go about it in the future?

As founders, we are all aiming to build large, scalable businesses. It is important to realize that scale, especially in fintech, can only be achieved within the ambit of a regulatory framework. When it comes to investing money, the most important thing for the user is trust. Obtaining a SEBI license to offer investment options is the most critical way to establish that trust.

From our experience, we have also realized that being regulated unlocks other significant tools and possibilities. In our case, it allowed us to integrate with the National Stock Exchange (NSE) to offer easier payment flows, engage credit rating agencies to provide an external credit rating to our investment instruments, use demat accounts etc. The cost of obtaining and maintaining the regulation pales in comparison to the business upsides.

We have established a dedicated legal & compliance team and invested substantial tech effort in ensuring that we are fully compliant. At the same time, we actively engage with the regulator and concerned bodies to discuss aspects that would improve customer experience and safety. Grip is also a founding member of the Association of OBPP members and makes frequent representations to SEBI that would be in the collective interest of this industry. We have found the regulator to be open to constructive discussions in achieving the dual objectives of market growth and investor protection.

As a founder, what’s your vision for Grip over the next 5-7 years? What are the key levers that will take you there?

Grip will be to alternative fixed-income what HDFC was to FDs and Zerodha to equities. That is our vision for the business. On the back of an established regulatory framework, an exciting suite of products, and an incredible team, our focus is to consistently deliver on our brand promise and customer experience. We are fortunate to be building in a macro environment for rapid growth in India and a micro set-up where users and businesses are challenging the 30-year status quo of having just two investment options.

Share this post

Share this post