From Private to Public: Top Considerations as Startups Navigate the IPO Playbook

published By Nidhi Duggal , June 7, 2024

In recent years, India’s economic landscape has been marked by the rise of startups and the proliferation of innovative ventures across various sectors. As these enterprises mature, many contemplate taking the next significant step in their journey: going public through an Initial Public Offering (IPO). An IPO not only provides access to capital but also establishes a company’s presence in the public market, offering liquidity to early investors and potentially unlocking new avenues for growth.

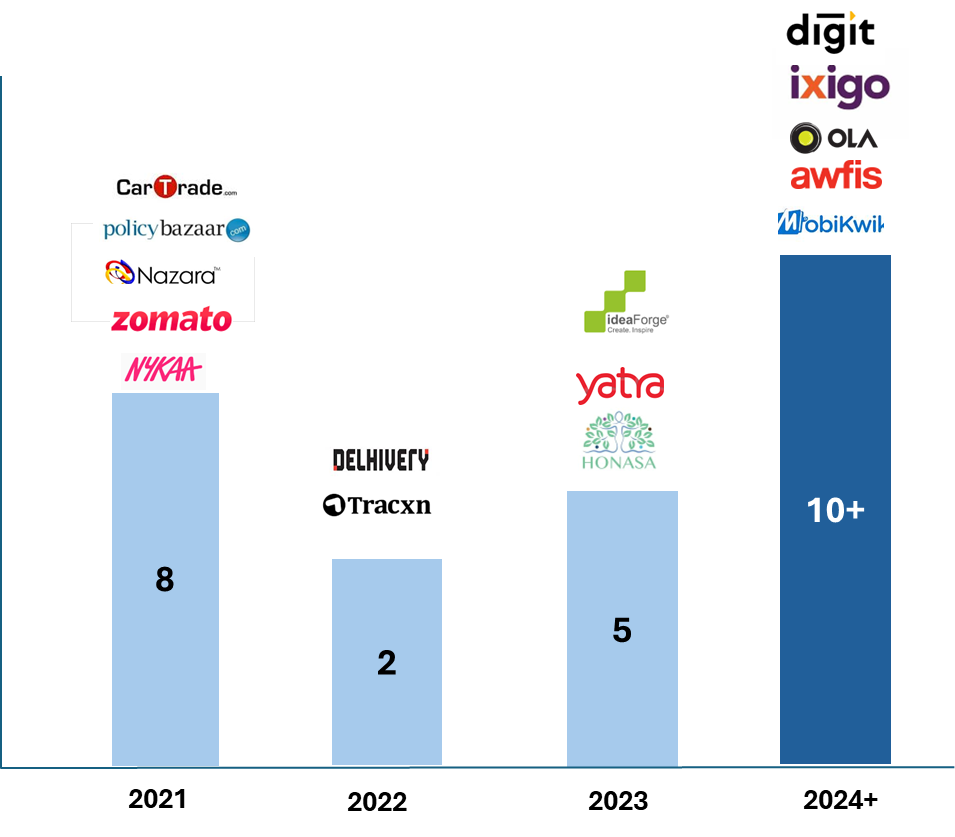

Since 2021, ~15 startups have tread the listing journey successfully with market cap varying from $75M to $12B at the time of listing. With ~25 startups expected to list in the next 18-24 months and many more sitting on the fence aspiring for it, this article is aimed to provide a broad guidance on decisions that the stakeholders need to make in order to achieve the aspirational goal of listing.

Need: Why aim to list?

In a conversation with Neha, co-founder at Tracxn, she shared that in 2013, while she was at Stanford, she and Abhishek envisioned creating a global data platform to provide market intelligence on private companies. They chose to incorporate in India since they desired to create an ‘India Listing Story’. Eight years later, Tracxn went public on the Indian stock exchanges. What struck me was the clear intent of going public even before incorporating the company.

Founders that start with a listing mindset want to create something that outlasts them. “Public” signifies a level of accomplishment, evolution and a deep sense of commitment which is hard to achieve as a private company.

By targeting an IPO, the founders enhance the likelihood of developing a business that can achieve profitability, scale, growth, and generate long-term value.

Listing also fosters independence and professionalization in the company’s operations, governance, and management. This professionalization contributes to creating a more robust and sustainable organization.

Applicability: Is listing good for ALL startups?

The Indian IPO landscape has undergone a significant shift. Traditionally, companies seeking IPOs were established, cash-generating businesses in manufacturing or large, regulated sectors like banking and insurance. These businesses were often bootstrapped and boasted long track records, typically exceeding 20 years before going public.

However, the internet revolution has spurred a new generation of companies: tech-driven, capital-light startups. These “new-age” ventures, many founded around a decade ago, are now challenging the traditional path to an IPO. They are seeking listings based on a combination of financial and non-financial metrics, reflecting the unique nature of their innovative business models. This shift has also prompted the regulatory body, SEBI, to adapt its processes to accommodate these new-age companies. So, what is the MVR to list a company?

- Established Businesses: Startups should ideally have a 3 year due-diligenced track record of financial performance, preferably under the same company name, at the time of applying for listing.

- Sustainable Business Model: Around 60% of startups listed in the last 3 years were not profitable at the time of listing. SEBI does not necessarily require a startup to be profitable but it must have a sustainable business model with a line of sight to profitability. Loss-making startups like Zomato, Delhivery, and Nykaa have successfully listed by demonstrating their strong growth prospects and market dominance

- Clear business plan & vision: The regulator needs to get comfortable with the ‘Use of proceeds’ disclosed in the DHRP. SEBI permits companies to allocate a portion of the IPO funds (typically up to 25%) for “general corporate purposes.” However, actual use of all IPO proceeds need to be disclosed in the issue documents and reported until the funds are exhausted.

- Steady & growing non-financial parameters – For new-age companies, GMV, # of customers, EBITDA are more important than Revenue & PAT. Current rules require the companies to share non-financial metrics and their growth percentages for the last 3 years.

- Capital Requirements: Companies that require substantial capital for expansion, acquisitions, research and development, or debt repayment benefit from an IPO. Going public provides access to a broader investor base and capital markets to meet these financial needs.

- Availability of Valuation benchmarks: For category creating companies, like MapmyIndia, Nykaa, which provide a niche service/product, finding direct domestic competitors for valuation can be difficult. This challenge becomes even more pronounced for loss-making startups seeking an IPO. Therefore, SEBI relies on benchmarking with similar international players based on non-financial metrics like consumer base, product advantages (moat), and features.

- Regulated sector finds it easier: A regulated NBFC or BFSI would find it easier get SEBI approval as long as they have the other requirements in place

Stage: When should a startup think about listing?

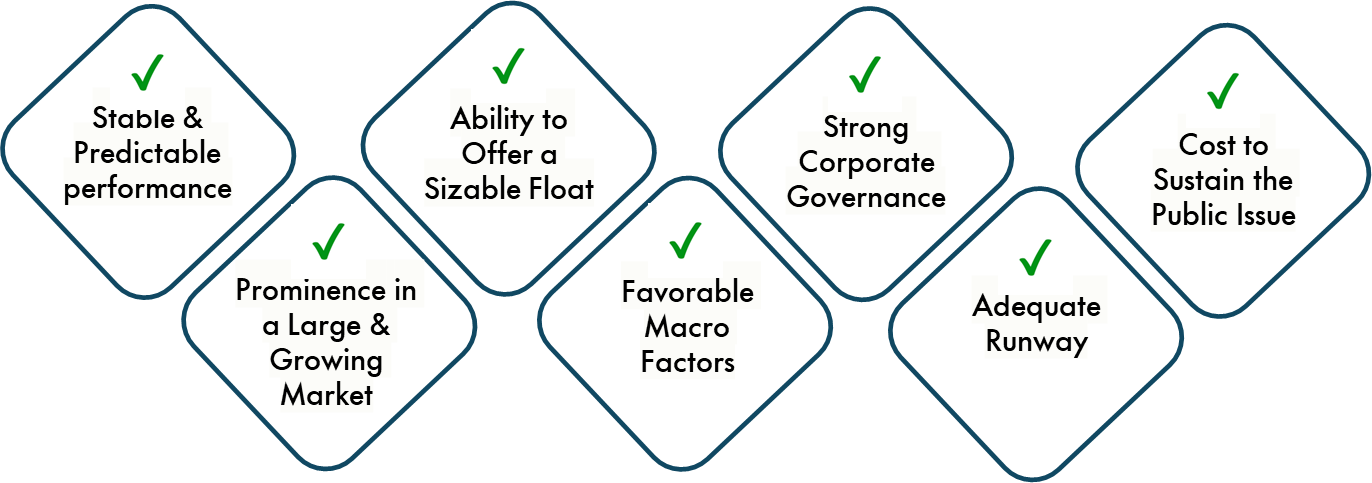

A few years ago, a founder would have been considered ambitious if they started aiming for IPO post raising Series C/D funding. However, the successful listing of Mamaearth, Nykaa has shown that an IPO can be a tangible goal. While external macro factors which are beyond the control of the founder can always play a role, a founder should carefully consider the readiness and maturity of the company when planning an IPO.

A startup can think about listing when it has achieved stable performance, meaningful scale, and growing metrics that can be predicted with a fair degree of certainty. Even if the startup is loss-making, it should aim to achieve EBITDA profitability before listing. The business should be a category leader in a large and growing market to give investors confidence to hold the stock long-term, and it should be able to present a compelling vision for the next 5-6 years.

The ability to offer a sizable float is crucial, as regulatory requirements mandate that 25% of the overall shareholding must be owned by the public, not held by promoters or related parties, to justify the IPO process (either at the IPO itself, or within a 3-year runway for large capitalized companies) – whether via Primary Issue, Offer for Sale (OFS), or a combination of both. For instance, if a company aims for a $100 million IPO with a 25% public float, the post-issue valuation would need to be $400 million. The float size should be meaningful to attract long-term institutional investors who can weather business cycles and provide sufficient liquidity for post-IPO sell-downs.

While timing the market is challenging, companies planning an IPO should assess economic tailwinds, investor demand, and market trends. Many startup IPOs, such as those of Zomato, Nykaa, and PolicyBazaar, were launched in 2021 when liquidity was high, investor sentiment was positive, and market conditions were favorable.

To be ready for the financial and regulatory rigor required for listing, a business needs to achieve maturity in governance and management, ensuring increased transparency and accountability through regular financial reporting and disclosure requirements. Additionally, once the IPO process is underway, Pre-IPO rounds should be priced with the eventual IPO valuation in mind to prevent material discrepancies and SEBI queries.

Finally, startups should have adequate runway since IPO processes are time-consuming and involve substantial costs, including underwriting fees, due diligence, legal expenses, and compliance costs, which can range between 3-7% based on regulatory approvals and the complexity of the offering.

Regulator: What do they seek?

The duty of SEBI is to

“ …to protect the interests of investors in securities and to promote the development of, and to regulate the securities market and for matters connected there with or incidental there to“.

India has significantly higher participation of direct retail investors in IPOs, leading to SEBI’s rules designed to protect small investors. The regulator has published stringent and exhaustive rules for disclosure of financial performance standards, offering information, and risk factors to encourage transparency and better corporate governance in the LODR Regulations (along with applicable updates). The intent is to ensure that there is no misstatement in the offer to the public or any misinformation that can generate future liability for the company. During the review process, SEBI meticulously examines the offer documents and may request additional disclosures, clarifications, or adjustments regarding related-party transactions or governance lapses.

If the regulator is not satisfied with the provided information, it may defer the IPO application, requiring the company to address any deficiencies or provide additional disclosures. This can delay the IPO process, but SEBI typically does not reject the application entirely. In contrast, the US regulatory body also requests additional information, but it does not typically defer or return IPO applications as frequently as SEBI.

Jurisdiction: Is it better to list in India vs the US?

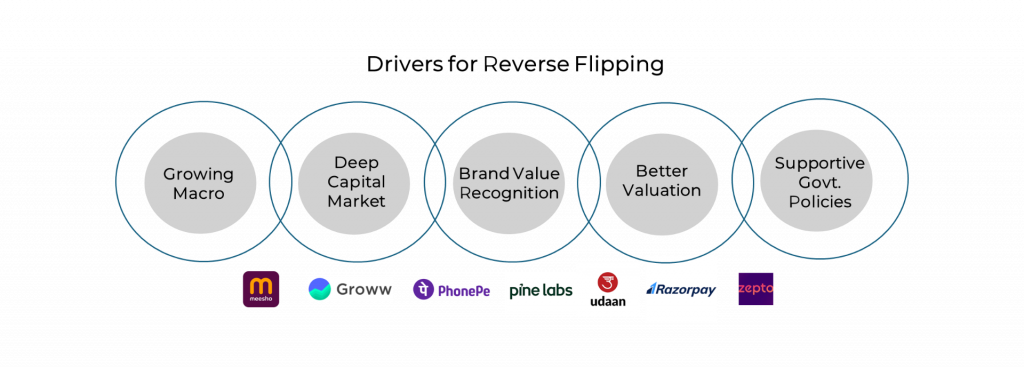

In a surprising reversal of trends, many established startups with overseas headquarters are now setting their sights on listing domestically in India. This shift comes despite significant costs and tax challenges involved.

SEBI’s recent efforts to streamline the listing process and adopt best practices from other markets have significantly eased the path for startups in India. Notably, the UK’s principle-based disclosures focus on fair and accurate reporting, while the US employs stricter definitions and prescribed criteria for valuation parameters. India’s LODR Regulations borrow the US concept of minimum listing requirements while emphasizing fair disclosures, creating a balanced approach.

Beyond the streamlined regulatory landscape, India offers several other compelling factors that are attracting startups back home.

India offers a compelling proposition for startups considering an IPO, with its growing economy, resilient political stability, and a maturing retail investor base that now understands the complex business models of new-age companies. Recent startup IPOs in India have seen strong retail demand, demonstrating this shift. For e-commerce, fintech and broking firms that derive most of their value domestically, listing in India provides greater brand recognition and relatability with Indian investors. Indian startups can potentially achieve higher valuations (at – least 30-50% higher multiples) in the domestic market due to scarcity premium and stronger brand recall. SaaS businesses are following the trend since listing in India is less competitive – for instance, compared to the US where a $300 million annual revenue is often expected, SaaS companies in India can access the public market earlier with just $125 million in revenue. The Indian government has also introduced supportive policies, like the GIFT City listing committee’s focus on “onshoring Indian innovation,” to further solidify the favorable environment for domestic listings. Hence, startups with strong unit economics and predictable growth stand to benefit substantially from listing in India.

Promoter rights & obligations: How do they change at the time of an IPO?

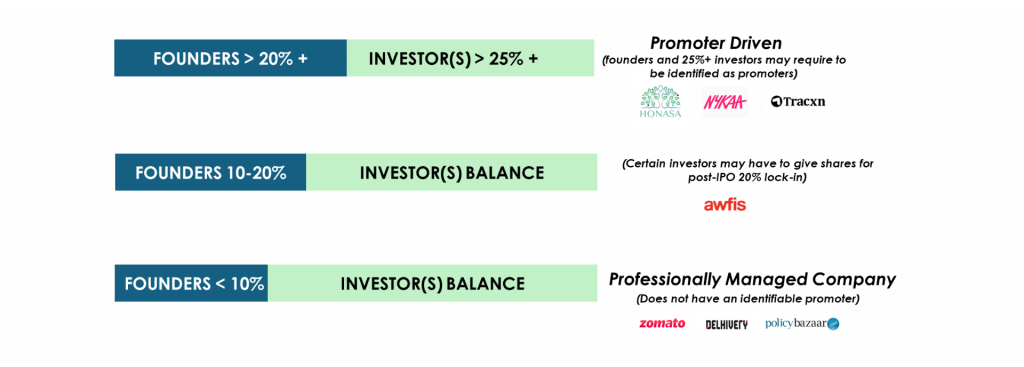

One of the most important decisions in preparing for an IPO is to determine the classification of the company based on ICDR rules – whether to float as a Promoter Driven company or Professionally Managed Companies (PMC).

The process of identifying Promoters has become complex recently, with the stock exchanges providing some (unwritten) guidance on the matter. Hence, identifying Promoters must be done on a case-by-case basis, considering a myriad of factors.

If the founder or an investor group holds more than 25% shareholding post-IPO, the company is likely to be classified as a Promoter Driven Company (PDC). In such cases, promoters undertake the liability for offer document disclosures (and the accuracy of the information), post-listing obligations (such as maintaining minimum public shareholding and adhering to corporate governance practices), and 20% of the post-IPO holding of identified promoters is locked in for 1.5-3 years. SEBI, in a directive on May 29, stated that no special rights can be retained by any shareholders in an IPO-bound company. Any post-IPO special rights would have to be taken up post-listing and not during the listing process.

If an IPO bound company wants to file as a professionally managed company, it would need to consider multiple steps before filing, including (a) paring down founder shareholding, (b) having founders potentially give up board-rights, (c) analyzing post-Offer shareholding and structuring the Offer to bring down investors below the bright-line thresholds (usually 25%), and (d) ensuring that annual returns and other documents reflect the PMC status. Institutional investors holding significant shareholding (>20%) also usually sell all or most of their holding in an Offer for Sale (OFS) to safeguard themselves from liability on offer documents; for example, Softbank sold 22.78% as part of Delhivery‘s OFS. If there is no single controlling shareholder or group, and the management is professionalized, the company may be classified as a Professionally Managed Company (PMC). This classification generally signifies a more diffused ownership structure with no dominant promoter(s).

Existing Investors: How are they impacted?

For existing investors, an IPO presents both exciting opportunities, and important considerations. A successful IPO creates a liquidity event, allowing investors to monetize their investments and potentially generate significant returns. However, the liquidity is subject to lock-in periods to restrict early selling after the IPO to ensure market stability. A few critical aspects from the point of view of institutional investors are:

- Conversion: The company’s cap-table needs to be cleaned up and frozen at the time of Draft Red Herring Prospectus (DHRP) and the convertible shares will convert into equity shares. The converted equity shares would be locked in for 6 months post listing

- Dilution: Existing shareholders may experience dilution of their ownership percentage as new shares are issued and sold to the public.

- Rights: Shareholders’ Agreements terminate upon listing and special rights held by investors (e.g., veto rights, special voting rights) are to be removed from the Articles of Association at the time of listing.

- OFS Eligibility – Shares that have been held for at least one year become eligible for inclusion in an Offer for Sale (OFS). This provides a valuable exit route for long-term investors, allowing them to sell a portion of their holdings during the IPO. Importantly, selling shareholders are restricted from participating in pricing decisions directly or through the IPO committee, ensuring a fair and transparent pricing process for all investors.

Post-IPO: What changes to expect?

An IPO transcends mere financial transactions; it is a strategic milestone with profound implications. Following an IPO, a company gains the capacity to raise significant capital, fueling growth initiatives, R&D, marketing endeavors, and strategic acquisitions. Publicly traded shares offer heightened liquidity and valuation, empowering companies to leverage their stock for M&A activities. Going public elevates a company’s visibility, credibility, and brand recognition among stakeholders while preserving its corporate identity. Public firms can incentivize talent retention through stock options and discounted purchase plans, enabling employees to realize the value of their investments in the public market. However, the transition to a public entity entails stringent regulatory and compliance obligations, entailing increased costs and time dedicated to adherence, reporting, and legal matters. Establishing specialized committees for audit, compensation, and disclosure ensures fairness and transparency. Public companies face the imperative of delivering consistent quarterly results, meeting market expectations, and navigating market volatility. Embracing a long-term perspective alleviates the pressure from stock-price fluctuations and external influences.

Successfully navigating an IPO underscores a company’s resilience under intense scrutiny and pressure. In essence, an IPO signifies a transformative juncture for companies aspiring to expand operations and access capital markets in India. While the IPO journey presents complexities and hurdles, triumphant IPOs can ignite growth, amplify visibility, and generate value for stakeholders. Companies embarking on the IPO process must approach it with meticulous planning, diligence, and transparency to navigate regulatory landscapes, mitigate risks, and seize the opportunities inherent in India’s dynamic market environment.

Share this post

Share this post